Why the smartest approach to keep assets safe is to leverage existing infrastructure

Hello everyone, and welcome back to The Ecosmic Compiler! It’s been a while, we’ve been busy with a lot of exciting things happening. We hope your year kicked off just as strongly.

I’m Ruggero, I look after strategy and finance at Ecosmic. Which means I spend a lot of time asking a simple question: does this actually make economic sense?

In space, that question can be… inconvenient.

Because the default answer is often:

“Maybe in the future. If everything goes well…”

This is especially true when it comes to building infrastructure. And in Space Domain Awareness, the go-to strategy has been pretty consistent: build infrastructure.

Need tracking? Build sensors.

Need more coverage? More sensors.

Need better data? You know the drill.

Very cool. Very expensive. Not always very smart.

So the natural question becomes: do the numbers actually make sense? Or, as real finance bros would say: does the business model work? Good question…

So at Ecosmic, we started asking ourselves: is there another way to do this? Is there a way to build a leading SDA company without spending tens of millions on infrastructure? Is there a way to build a scalable and profitable SDA company?

That’s what this edition is about: winning SDA without owning sensors.

The traditional way: own the sensors

There’s a logic to it.

If data is “the new gold”, owning the infrastructure that produces it sounds like a great choice. Build your radars, telescopes, RF networks, maybe even space-based sensors, and you control the full stack.

On paper: perfect.

In reality: long, painful and expensive.

Sensor networks are not a side project. They take years to build, serious capital, and global operations just to become useful. And once you build them, congratulations, you now also own:

- huge upfront costs

- ongoing operational costs

- long deployment timelines

- the need to build a full network as one sensor alone is not enough

- regulatory and legal headaches across multiple countries

- and a business model that needs to justify all of the above

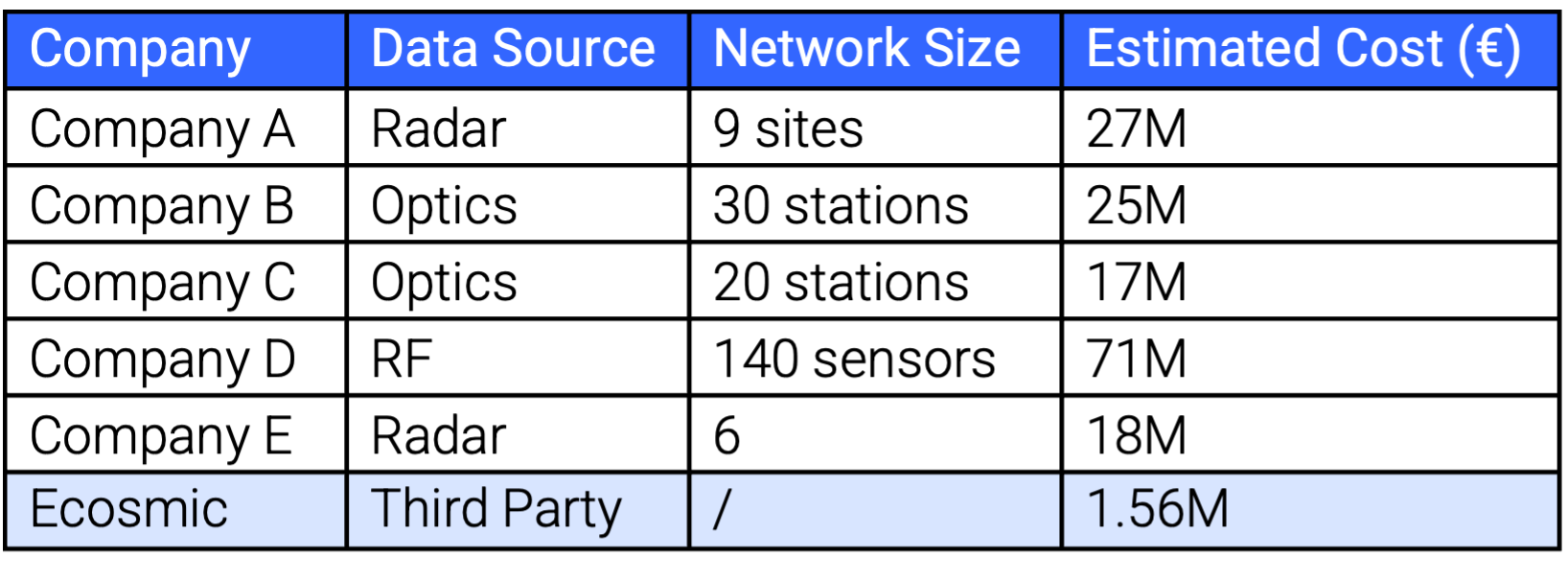

If you like numbers just as much as us, here is a quick comparison between building sensor networks1 and using third party data:2

Data is becoming a Commodity, Intelligence is the product

Now the fun part.

SDA data is not as scarce as it used to be. There are:

- public/semi-public catalogues

- commercial radar, optical and RF data providers (tracking objects through radiofrequency signals)

- operators with telemetry

- satellites carrying sensors

In fact, if we look at the data,3 one thing becomes clear: both ground-based and space-based sensors are already everywhere.

Today, more than 1,030 ground-based SDA sensors are active worldwide, operated by stakeholders across 40+ countries. Europe alone hosts 242 sensors, more than any other region, including North America. And the trend is not slowing down, in February 2025 (month in which this data was published), 90 additional ground-based sensors had already been announced, with hundreds more expected in the coming years.

And it’s not just happening on the ground. In orbit, the trend is accelerating. Between 2024 and 2033, more than 230 space-based SDA satellites are expected to be launched by more than 40 different companies and/or agencies.

But this only captures dedicated SDA assets. Today, there are more than 15,000 active satellites in orbit. Even after excluding SpaceX, which accounts for roughly 65% of the total, more than 5,000 satellites remain operated by a wide range of actors, most of which already carry sensors that could contribute to SDA. Nearly all satellites are equipped with star trackers, continuously imaging the sky, and even SpaceX is starting to leverage for Space Situational Awareness through its Stargaze initiative (you can ready more about it in the february issue of the Ecosmic Compiler). In parallel, many satellites host optical payloads (e.g. for Earth Observation) that can be partially repurposed.

Which means the volume, diversity, and availability of data in orbit is not just growing, it is already massively underutilised and will only continue to expand.

At some point we started realising something:

The sensor network already exists, it’s just… not owned by one player but distributed among many. And it’s getting bigger and bigger everyday. Data is not scarce anymore.

If data is increasingly available, then the bottleneck moves.

Not to collecting data but to making sense of it.

Data is becoming a commodity, intelligence is the real product.

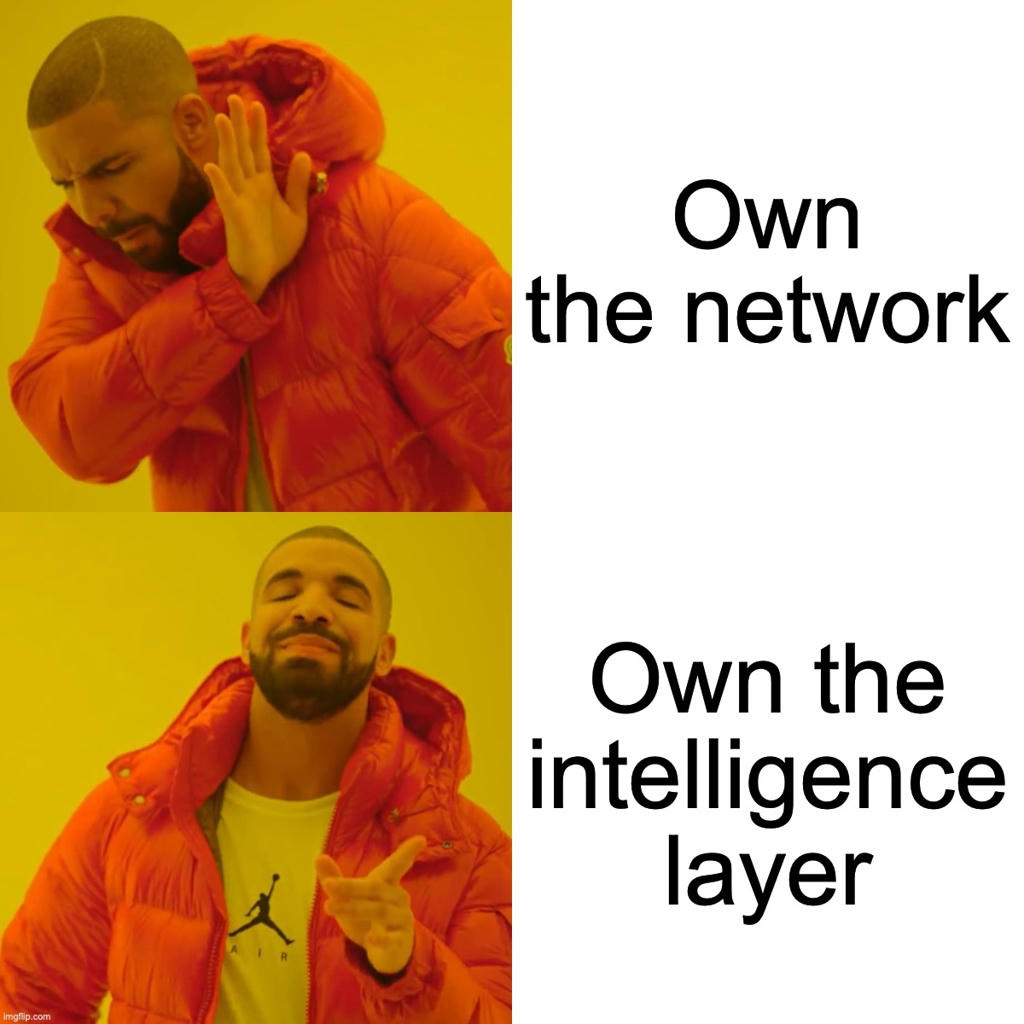

Actual slide that came out from the Founders’ strategy meeting:

The Ecosmic way: don’t own the sensors, own the intelligence layer

At Ecosmic, our bet is simple, yet revolutionary for the industry: you don’t need to own sensors to win SDA, you need to provide intelligence better than anyone else.

This means: building the best data orchestration layer, developing the best algorithms and delivering intelligence that actually drives decisions.

Instead of building infrastructure:

- we source data from multiple providers

- combine different sensor types

- integrate customer data when available

- build a shared data layer across products

Why? Because it’s more capital-efficient, more flexible and more scalable.

One data source is weak? Use another. A new provider appears? Integrate it

We’re building the data-fusion layer that makes sense of all of them.

And the great news? The business model actually seems to work…

Cool. So all companies will be the same?

Not really. The differentiator, or what our cool VC friends like to call the MOAT, is not in owning the biggest sensor network but rather in:

- the quality of your data fusion layer

- the performance of your algorithms

- the ability to turn intelligence into decisions

This is where the SDA battle will be fought. Ecosmic is ready to fight.

Closing thought

In strategy, every investment is a bet on what kind of company you want to become.

Owning sensors is a bet that advantage comes from collecting and owning data.

Our bet is different. At Ecosmic, we think our advantage comes from staying flexible, having multiple providers and building the best intelligence layer on the market.

Or, in finance terms:

don’t spend millions building telescopes for better data if what the market really needs is better answers.

Ruggero

Come find us

If you’re reading this from the Space Symposium, you’re in luck! Our CEO Benedetta and CCO Imane are in Colorado Springs right now representing Ecosmic at one of the year’s most important space industry events. Don’t hesitate to get in touch to arrange a meeting on the conference floor or at one of Space Symposium’s many afterworks.

If you don’t catch us there, we’ll be at SmallSat Europe on May 26 to 28, with many more events coming up over the summer.

1 Ecosmic elaboration based on information and data from: Novaspace (2025, April). Space Situational and Domain Awareness – A global outlook of activities, investments and trends in Space Situational and Domain Awareness.

2 Our estimate for data costs related to R&D and COGS for multiple products covering hundreds of satellites

3 ”Space Situational and Domain Awareness: A global outlook of activities, investments and trends in Space Situational and Domain Awareness” ; Novaspace; April 2025